RMI has argued for some time that the energy transition is possible today and requires no new technologies.

In 2014, Reinventing Fire mapped a path to greater than 80 percent reductions in carbon emissions, at a cost $5 trillion cheaper than business as usual, while requiring “no new inventions.” Six years later the deployment of some technologies—including solar and wind, battery storage and electric vehicles—is accelerating faster than many believed was possible.

But many other technologies identified in that book, particularly those at an early stage, are either stuck in the lab and university or with only limited deployment—e.g., low-carbon steel and cement, advanced evaporative cooling; smart windows, phase change materials; and alternative electric motor designs. Climate tech needs a faster and more reliable path to market. And even if we don’t need wholly new inventions, they certainly wouldn’t hurt either.

RMI just launched Third Derivative (D3), a new climate tech accelerator, in order to address this technology-to-market bottleneck. This blog will identify some of the most important opportunities for innovation in order to get on track for a pathway to keep global temperature rise limited to 1.5°C.

Progress to Date

In the past 10 years, solar PV costs have dropped by ~90 percent, wind power by ~70 percent, batteries by 80 percent, and LEDs by 85 percent, creating both a financial and environmental case for switching to these clean energy solutions. Without these technologies emissions would be 1.25 Gt higher per year.

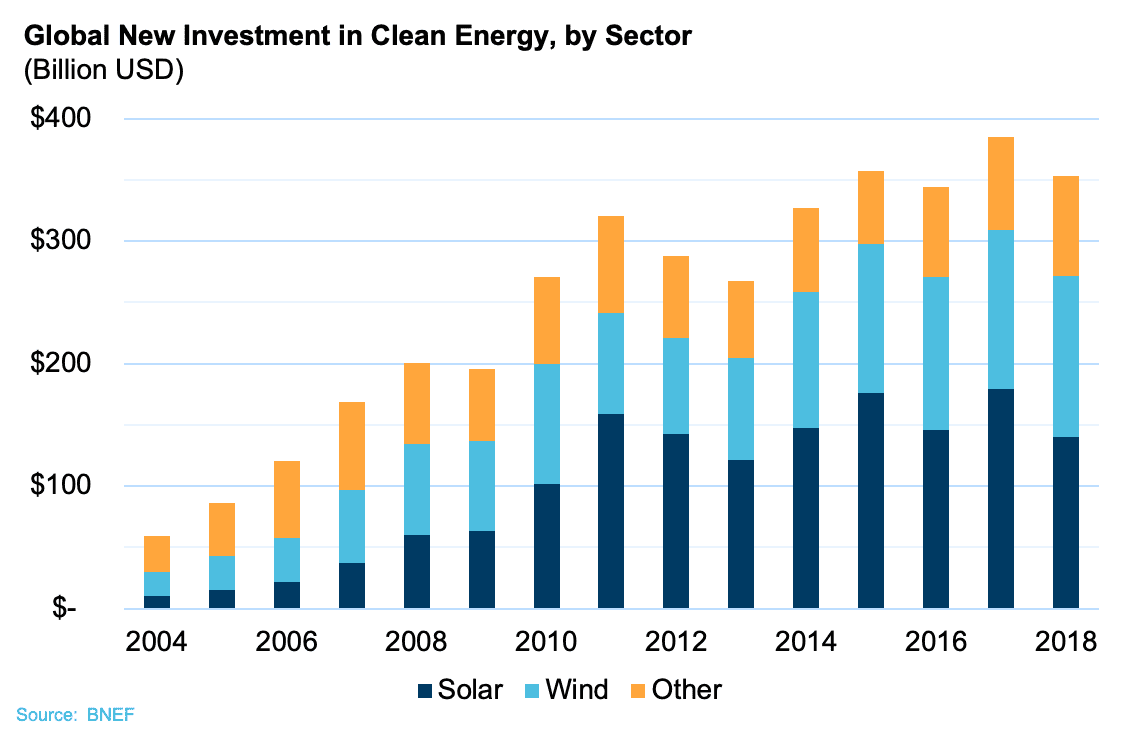

The cost of these mature technologies now competes with conventional generation, even as government subsidies are reduced. In many places they are now the cheapest option and are attracting strong investment (Exhibit 1). This creates a virtuous cycle of increasing scale and further refinement of technology, manufacturing processes, and streamlined deployment which then leads to further cost reduction and additional investment. Batteries and electric vehicles are approaching or have perhaps passed similar tipping points.

Clean energy investment overall has now reached $300 billion per year, mostly for wind and solar power. This is at least on the same order of magnitude with what most research suggests is needed to decarbonize for the electricity sector, which is responsible for almost 30 percent of global carbon emissions.

Innovation gaps and opportunities

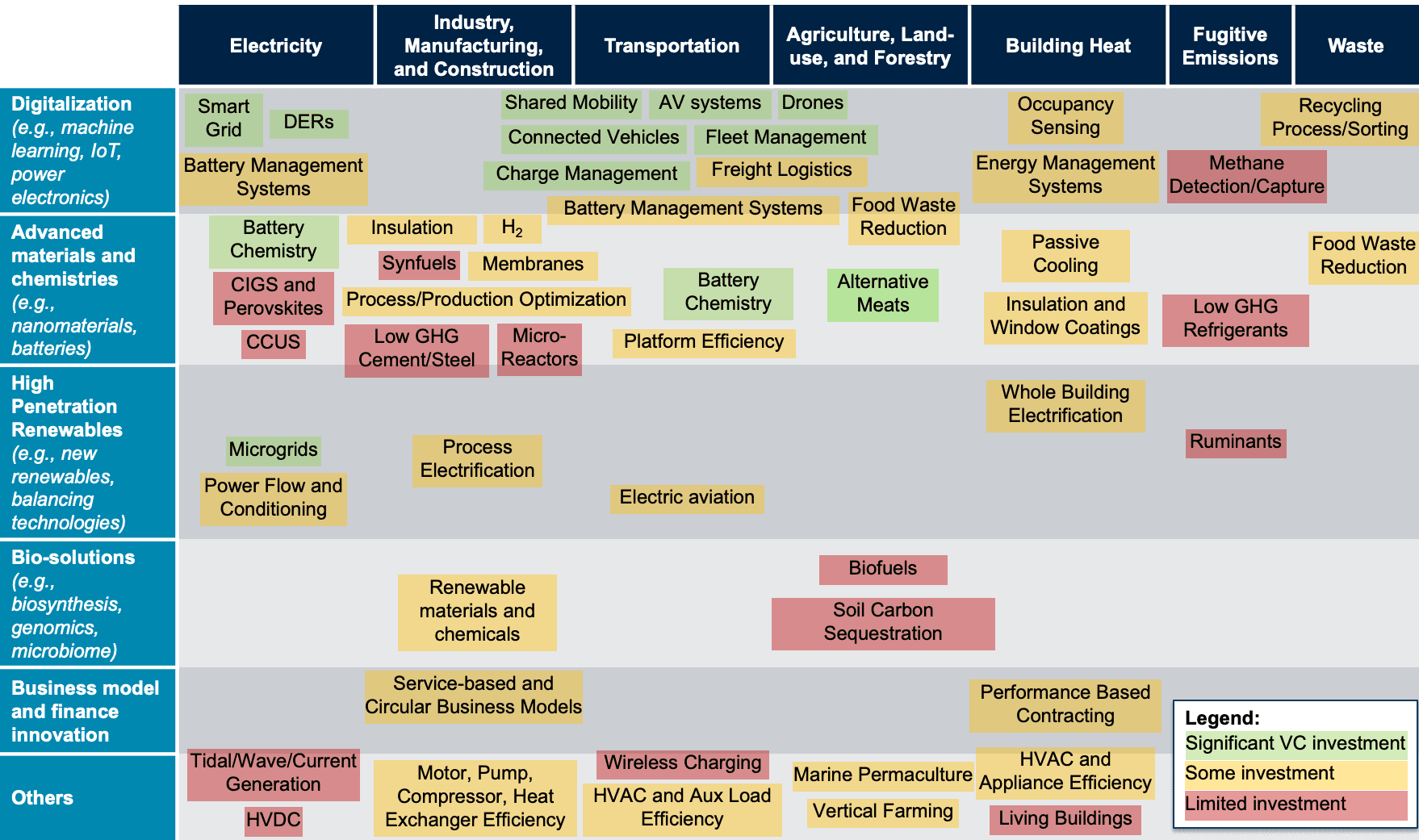

But very little progress has been made in other climate tech sectors, sometimes called “hard-to-abate,” which are responsible for more than two thirds of current GHG emissions (Exhibit 2). These hard-to-abate sectors attracted less than $1B climate tech investment in 2019, partially because technologies in these sectors are less mature.

Even in the electricity sector, further innovation is needed to balance the grid when wind, solar, and other variable renewables are not available (especially seasonal or long duration storage). Key challenges in other sectors include long-distance transportation (especially freight and aviation) and heavy industry.

Thankfully, there is no shortage of promising ideas and new technologies for addressing carbon emissions across these hard-to-abate sectors and the rest of the economy. RMI has surveyed government and university labs focused on energy and manufacturing process innovation as well as tech transfer programs like ARPA-e to identify some of the leading ideas across major energy sectors (Exhibit 3).

Most of these have the potential to be cost-effective against current approaches and could scale rapidly. Some of the most important new technologies—like advanced batteries, synfuels, and hydrogen—are cross-cutting and enable emissions reduction across multiple sectors.

Entrepreneurs and early-stage investors are already working to take some of these ideas from the lab and develop real-world applications with a scalable business model, but progress is slow and many important technologies are still stuck.

Most researchers agree that carbon emissions must be cut dramatically over the next ten years in order to avoid some of the worst consequences from climate change.

These early-stage technologies, critical for hard-to-abate sectors, can take 5–10 years of development and early adoption before they are ready for widespread deployment, even with adequate investment and other support. However, venture investment into climate tech struggles compared with sectors like medtech, creating a major obstacle to fighting climate change.

The time to change this is now, and RMI has launched Third Derivative to speed the way.

In the next blog we will look more closely at some of the specific barriers along the way that either slow or block progress commercializing early-stage technology.